Jack In The Box (NASDAQ:JACK) is a leading fast food company operating restaurants under its namesake brand and it also owns Del Taco which offers Mexican-style fast food. The fast food industry has been facing a number of challenges which include rising labor costs, rising food prices, as well as some recent spending weakness with lower end consumers. There is also significant competition from other fast food companies, many of which are increasing value type deals. All of this has taken a toll on the share price of JACK, and the stock has been cut in half from the highs it held in 2023. This has motivated me to take a closer look in order to see if there is a buying opportunity at hand.

There are a number of signs that suggest that the selloff has gone too far, and the stock looks deeply undervalued now after a 50% drop from 2023 highs. The price to earnings ratio is extremely low which indicates potential undervaluation and this stock now offers an attractive yield of roughly 3.5%, which could also suggest it is undervalued. The longer term charts are also signaling undervaluation and a potential buying opportunity. Furthermore, there are a number of potential future growth drivers, including domestic and international expansion. This company also has earnings growth drivers which include cost cutting and share buybacks. Let’s take a closer look.

The Chart

If we look at the long term chart of Jack In The Box below, it gives us some perspective in terms of historical buying opportunities. The chart shows that this stock plunged to around $32 during the Covid stock market correction in 2020. The stock ended up surging from that level and roughly tripled in value when it traded for around $120 per share, in the following year. In 2023, the highs for the share price were around $100, and the stock is now trading for half of that level. It’s worth noting that this stock has rarely traded at or below the 200-month simple moving average which is represented by the light brown trendline. Since 2012, the stock has only touched or gone below this level less than a handful of times. It went below this level during the Covid selloff, and it touched this trendline in 2022 and 2023, and right now it trades below it.

This shows that in the past 12 years or so, this stock has only dropped measurably below the 200-month simple moving average twice — once during the Covid stock market selloff and right now. Of course, it was a big buying opportunity back in 2020, and only time will tell if the opportunity today will play out the same way. However, it is very rare to even get a chance to buy below the 200-month moving average, so I believe this is probably another ideal buying opportunity.

Finviz.com

Earnings Estimates And The Balance Sheet

Analyst expectations for Jack In The Box are low in terms of revenue growth, but earnings are expected to see growth thanks to cost-cutting measures and lower food inflation. Analysts expect the company to earn $6.32 per share in 2024, on revenues of $1.59 billion. In 2025, earnings are expected to rise about 12.55% to $7.11 per share; however, revenues are expected to drop nearly 2% and come in at $1.56 billion. In 2026, revenues are expected to remain flat, but once again, earnings are expected to rise over 12%, with the company expected to earn $7.99 per share. These estimates suggest an incredibly low price to earnings multiple of about 8x earnings for 2024, and just about 6x earnings estimates for 2026.

By contrast, McDonald’s (MCD) is trading for about 21 times earnings and analysts are only expecting year over year growth of around 4% to 5% for the next couple of years and earnings are expected to grow at a slower pace than Jack In The Box.

As for the balance sheet, it has about $3.18 billion in debt and just over $20 million in cash. I don’t find the balance sheet to be very attractive, but the food business has very steady and consistent cash flow which helps to offset the levels of debt on the balance sheet. Furthermore, the company might reduce debt by refranchising or selling company owned stores.

The Dividend And Share Buybacks

The quarterly dividend is $0.44 per share, which totals $1.76 per share on an annual basis. With the recent share price decline, this stock is now yielding about 3.5%. That is an enticing yield, and it appears secure since the payout ratio is just about 29%. This yield will pay shareholders to patiently wait for a higher share price.

The company is also buying back shares, and during the second quarter of 2024, it repurchased about 200,000 shares for an aggregate cost of roughly $15 million. The company stated there is $210 million in authorized share buybacks remaining at the end of the second quarter. $210 million is very significant because it represents more than 20% of the current market capitalization which is just around $973 million.

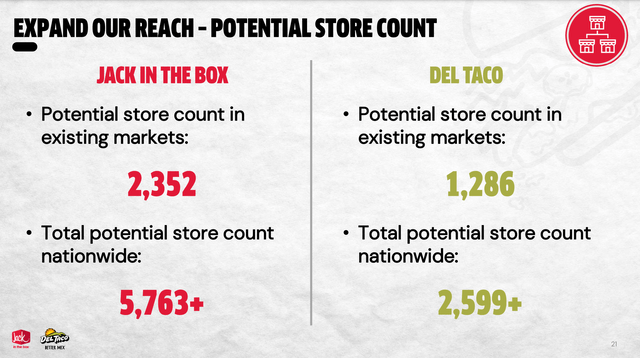

Jack In The Box And Del Taco Have Significant Expansion Potential

While analysts are expecting revenues to be relatively flat for the next couple of years, company management appears to see significant long term growth opportunities as shown in the graphic below. I believe this company has significant expansion potential overseas, but the company probably needs to focus on getting things right at home first.

Source: Jack In The Box

I See Positives That The Market Might Be Missing

Aside from the incredibly low valuation metrics, expansion potential domestically and internationally (the company has been opening new locations in Mexico), and the significant share buyback plan, there are other reasons to be more optimistic than what the share price currently seems to suggest. One of them could be innovation when it comes to menu offerings.

The “Smashed Jack” burger: In January, Jack in the Box introduced its first new burger in eight years, and this burger is touted as being a premium offering with the goal of it being the best burger in the industry. It put this new Smashed Jack burger on the menu (but didn’t do an advertising campaign) for a limited two-week run and it was extremely popular and sold out quickly through word-of-mouth. The company has planned to roll this new offering out nationally and it looks like it could have a very positive impact on revenues in the coming quarters and beyond. Here are some details on how successful the test rollout of this new burger was, as this Business Insider article states:

“Two weeks after launching, the Smashed Jack has become a fast-food unicorn. It’s nearly impossible to find as the chain ran out of supplies to make the specialized burger, which customers couldn’t get enough of. “We’re sold out,” Ryan Ostrom, Jack in the Box’s chief marketing officer, told reporters at a media event Wednesday at the chain’s San Diego headquarters.”

Potential Downside Risks

Management clearly has work to do to get costs down and get growth back on track, so I see management execution as a potential downside risk. Company executives also need to find creative solutions to remain competitive in this industry. I would also like to see management focus on paying down debt, because debt is more expensive now than it has been in years and it can be a potential downside risk as well.

The Del Taco acquisition has yet to be optimized in my opinion, so I see this as a potential downside risk. However, management is working to refranchise many Del Taco units whereby company-owned stores are bought by franchisees. This helps to make Jack In The Box a more asset-light company and it could help to reduce debt, as this process continues.

The lower end consumer is clearly under pressure and this is a market that Jack In The Box serves. Starbucks (SBUX) has even seen some pushback with signs that some consumers are becoming more cost conscious. In response to these changing market conditions, McDonald’s announced (in late June) that it would offer a $5 deal whereby customers could pick four items. This increases the competitive nature of this business and it could be a potential downside risk.

There’s another potential downside risk I see in the long term, and that is related to eating habits. There seems to be an ongoing trend towards healthier eating and that might negatively impact Jack In The Box, unless it starts to successfully introduce healthier food options. The other potential issue is that the growth of weight-loss drugs seems to be exploding and some analysts see this resulting in less food consumption in the coming years.

In Summary

This company clearly has challenges, but it also seems like these issues might already be priced in, and even more than priced in. At a price to earnings ratio that is about one-third of McDonald’s, this stock appears deeply undervalued. Investors who buy now will also get a 3.5% yield while waiting for a higher share price. In addition, as the charts show, this type of opportunity to buy the shares meaningfully below the 200-month simple moving average has only happened one other time and that was when Covid hit the stock market. That turned out to be a great buying opportunity and this could be as well.

I believe this company has growth drivers in terms of revenues through expansion, and growth drivers in terms of earnings through cost cutting and a significant share repurchase plan. Menu innovations such as the new “Smashed Jack” could also be potential future growth drivers.

With all of this in mind, I think it makes sense to take a small position and accumulate this stock over time in order to take advantage of any additional potential weakness in the share price.

No guarantees or representations are made. Hawkinvest is not a registered investment advisor and does not provide specific investment advice. The information is for informational purposes only. You should always consult a financial advisor.

Read the full article here